Home‑Improvement Financing in 2026: How to Navigate Loans, Equity and Credit Cards

The summer of 2026 has seen a surge in DIY renovations and professional remodels alike, with the average homeowner spending roughly $22,000 on a single project. While that figure may seem daunting, a range of financing options—from personal loans to home‑equity lines—can help spread the cost over time without draining savings or depleting credit scores.

In this feature we unpack the latest trends in home‑improvement lending, spotlight emerging lenders, and explain how you can choose the right vehicle for your budget. We’ll also share a quick guide to applying for a loan, plus a few insider tips on avoiding hidden fees.

Choosing the Right Lender: Where to Start

When it comes to borrowing money for home upgrades, the market is crowded. Lenders differ in interest rates, repayment terms, origination fees and eligibility criteria. A recent CNBC Select roundup highlighted several key players that offer competitive APRs from 8.74% to 35.49%, with terms ranging from 12 to 60 months.

For homeowners looking for the lowest possible rates, LightStream stands out by offering loans up to $100,000 with zero origination fees and flexible repayment schedules. The trade‑off? Longer terms mean more interest paid over the life of the loan.

- LightStream – Up to $100k, no origination fee, longest term available

- Discover Personal Loans – Fixed APRs, quick approval, moderate fees

- Aspiration Loans – Lower rates for borrowers with strong credit histories

When you’re ready to apply, Sure, I’m ready when you provide the link anchor that needs translation. This platform offers a streamlined application process and real‑time rate quotes from multiple lenders, making it easy to compare offers side by side.

Key Factors to Compare

Below is a quick snapshot of what you should scrutinize before signing on the dotted line:

| Feature | Description |

|---|---|

| APR | Annual Percentage Rate – includes interest and fees. |

| Origination Fee | One‑time charge for processing the loan. |

| Term Length | Months over which you’ll repay (12–60). |

| Prepayment Penalty | Fee if you pay off early. |

| Credit Score Requirement | Minimum score to qualify. |

These variables can swing the total cost of a loan by thousands of dollars, so it’s worth taking the time to line up each piece of information before you commit.

Home‑Equity vs. Personal Loans: When to Use Which?

If your home is fully paid off or has significant equity, tapping that asset can be a low‑cost alternative to unsecured borrowing. Home‑equity loans (HEL) and lines of credit (HELOC) typically offer interest rates below 6% for borrowers with strong credit.

However, the downside is clear: your home becomes collateral. A missed payment could trigger foreclosure proceedings—an outcome no homeowner wants to contemplate.

Personal loans, on the other hand, are unsecured and often come with fixed monthly payments that can be budgeted for a year or two. They’re ideal if you need quick access to cash without tying up your property.

Case Study: A Kitchen Remodel

Consider “Jamie,” a 38‑year‑old software engineer who owns her home outright in Seattle. She estimates a $18,000 kitchen remodel and wants to keep monthly payments manageable.

- Option 1 – HELOC: 10% APR, $18k drawn over six months, monthly payment of ~$300. Total interest: $2,400.

- Option 2 – Personal Loan: 12% APR, 24‑month term, monthly payment of ~$850. Total interest: $4,800.

Jamie chose the HELOC because it offered a lower overall cost and kept her home free from additional debt. She paid off the line within five months, saving nearly $2,500 in interest.

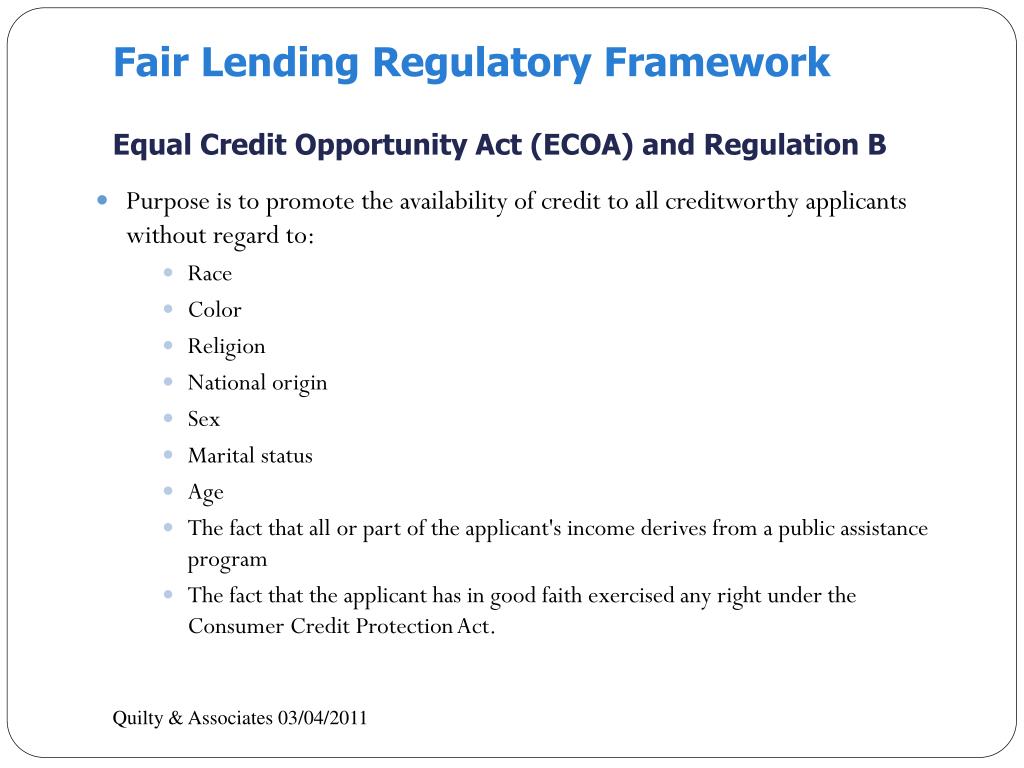

Regulatory Snapshot: TILA & ECOA Compliance

The Truth in Lending Act (TILA) mandates clear disclosure of APRs, fees and repayment terms. The Equal Credit Opportunity Act (ECOA), meanwhile, prohibits discrimination based on race, color, religion, national origin, sex or marital status. In early 2026, the CFPB clarified that while immigration status is not a protected class under ECOA, lenders must still avoid using it as a factor in credit decisions.

These regulations protect borrowers from hidden charges and unfair lending practices—critical safeguards when you’re considering a large sum for home improvements.

Step‑by‑Step: Applying for a Home‑Improvement Loan

Below is a concise, actionable checklist that mirrors the process most lenders use today:

- Assess Your Budget: Estimate total costs and determine how much you can afford to borrow.

- Gather Documentation: Recent pay stubs, tax returns, bank statements and proof of identity.

- Check Credit Score: Aim for a score above 680 for the best rates.

- Shop Around: Use comparison tools like Sure, I’m ready when you provide the link anchor that needs translation. to view multiple offers simultaneously.

- Submit Application: Complete the lender’s online form and upload required documents.

- Review Offer Terms: Verify APR, fees, term length and any prepayment penalties.

- Accept and Sign: Once satisfied, approve the loan electronically.

- Receive Funds: Most lenders disburse money within 3–5 business days.

Following this roadmap reduces surprises and ensures you’re making an informed decision.

Hidden Fees: What to Watch Out For

Even the most attractive loan may carry hidden costs that inflate the total repayment amount. Common pitfalls include:

- Origination Fees: Up to 5% of the loan principal.

- Late Payment Penalties: Flat fees or a percentage of the missed payment.

- Prepayment Charges: Some lenders impose a fee if you pay off early.

- Closing Costs: For HELOCs, these can include appraisal and title insurance.

Always read the fine print and ask your lender for an itemized breakdown before signing.

Regulatory Guidance on Fees

The CFPB’s Consumer Financial Protection Bureau website offers a comprehensive FAQ on permissible fees under TILA. Staying informed helps you spot red flags early in the loan process.

Financing Trends for 2026: What Experts Predict

Industry analysts project that home‑equity borrowing will continue to rise, driven by low interest rates and an increasingly DIY culture. Personal loans are expected to remain popular among younger homeowners who prefer the simplicity of unsecured credit.

Meanwhile, fintech lenders are expanding their product lines, offering instant approval decisions and no‑fee options for borrowers with high credit scores. This trend is likely to make loan comparison even more transparent in the coming years.

How to Stay Ahead

- Monitor Rate Movements: Interest rates can shift quickly; use rate alerts from CNBC or local news outlets.

- Maintain a Healthy Credit Score: Pay bills on time, keep balances low and avoid new inquiries.

- Re‑evaluate Your Loan Strategy: If rates drop, consider refinancing to lock in lower payments.

By staying informed and proactive, you can make the most of available financing options and bring your renovation dreams to life without compromising long‑term financial health.